Data monetization and hyper-personalization are redefining the banking and financial services industry. Transaction data has evolved from a compliance tool into a strategic asset that drives new revenue streams, boosts engagement by up to 40%, and strengthens trust through AI-powered personalization.

Hyper‑personalization goes beyond traditional segmentation or persona‑based targeting. It refers to the real‑time orchestration of data, AI, and contextual intelligence to deliver experiences, offers, and decisions individualized for customers across every interaction and channel. Unlike conventional personalization - which relies on static rules, historical attributes, and broad cohorts - hyper‑personalization continuously learns from live transactional behavior, intent signals, life cycle context, and environmental triggers. In financial services, this transforms transactional data into decision intelligence.

With the global data monetization market projected to grow from USD 4 billion in 2024 to USD 41.25 billion by 2034 at a CAGR of 25.8%, and digital transaction volumes continuing to surge worldwide, the opportunities for banks and payment providers are immense.

Why hyper personalization and monetization are necessary now

Changing customer expectations

74% of consumers want more tailored banking experiences, and 54% expect providers to leverage their financial data for personalization. More than 70% get frustrated when personalization isn’t delivered, while 76% are likely to engage if digital communications are personalized.

Competitive pressure from fintechs

Fintech investment reached USD 180 billion in 2023, intensifying the need for traditional banks to leverage their massive, proprietary data sets to stay competitive.

Margin compression

With average net interest margins declining by ~12% over the past five years, data monetization offers alternative revenue pathways. For example, one Asian bank generates USD 15 million annually by selling anonymized consumer spending insights.

The strategic imperative

Customer expectations are non-negotiable. Millennials and Gen Z - soon controlling trillions in annual income - gravitate to seamless, personalized digital journeys. Traditional institutions possess the richest transactional data sets; the imperative is to turn that data into value in real time.

Digital-native customer segment growth

Millennials and Gen Z - expected to amass USD 4 trillion in annual income by 2030 - prioritize seamless, personalized digital experiences.

Data proliferation and real-time analytics

The explosion of real-time transaction and behavioral data, enabled by AI/ML and cloud infrastructure, has paved the way for hyper-personalization.

Regulatory enablers

Open banking policies and frameworks promote secure sharing of granular financial data, which fuels hyper-personalized offerings.

Consumer acceptance of AI-driven insights

66 - 80% of consumers support using their data for personalized services and AI-based fraud detection.

Market landscape: The size of the prize

The BFSI vertical represented over 23% (~USD 5.2 billion) of the global data monetization market in 2024, heading toward USD 41.3 billion by 2034. Specifically for banking, the “Data Monetization for Banks” segment was USD 3.85 billion in 2024, with a 17.2% CAGR expected to reach USD 15.5 billion by 2033.

Hyper-personalization

The global market was estimated at USD 6.8 billion in 2024 for banking-specific applications, with a projected CAGR of 20.7% through 2033, reaching USD 44.4 billion. More broadly, the hyper-personalization market is set to grow from USD 21.2 billion in 2024 to USD 67.9 billion by 2031 (CAGR ~18%) across industries including BFSI.

Data monetization

The global data monetization market was USD 3.24 billion in 2023, expected to grow at ~26% CAGR to USD 16 billion by 2030.

As financial institutions seek new growth levers, the convergence of data and technology is reshaping the industry. Artificial intelligence (AI) and machine learning (ML) are no longer optional - they are the engines powering hyper-personalization and unlocking monetization at scale. These technologies enable real-time insights, predictive modeling, and autonomous decision-making, creating the foundation for next-generation experiences. This evolution is paving the way for agentic commerce - where AI-driven agents act on behalf of customers - and elevates the importance of consent management to ensure trust and compliance in a data-rich ecosystem.

AI and agentic commerce: Game changers

While market opportunities and drive prove compelling, artificial intelligence is the linchpin of hyper-personalization and monetization. It enables:

Real-time personalization

Citibank’s AI-driven merchant discount programs boosted card spend by 25% through instant offer delivery based on transaction behavior.

Predictive analytics

AI models forecast customer needs, enabling proactive product recommendations. McKinsey estimates predictive personalization can lift cross-sell rates by 10 - 15%.

Fraud prevention

Mastercard’s AI-powered fraud monitoring reduced fraud losses by 40%, while cutting false positives by 20%, improving trust and customer experience.

Formerly, personalization efforts were largely batch‑driven and retrospective, relying on static segments and delayed insights. Hyper‑personalization in the AI world, fundamentally changes this by embedding AI‑driven decisions directly into transactions and journeys in near-real-time. Instead of overlaying personalization on top of operations, institutions now make personalization native to underwriting, payments, risk, and engagement - driving materially higher impact across revenue, experience, and trust.

Looking ahead, agentic AI - autonomous agents that act on behalf of customers - will revolutionize commerce. These agents will dynamically deliver contextual offers, manage consent seamlessly, and optimize the customer journey. In agentic commerce, AI agents will autonomously execute transactions, creating frictionless, hyper-personalized experiences that blend convenience with trust.

Trust at the core: Consent management

In the era of data-driven personalization, consent management has emerged as the cornerstone of trust between financial institutions and their customers. As banks and payment providers increasingly rely on algorithms to generate insights and deliver hyper-personalized experiences, the responsible collection, storage, and usage of customer consent determines both the ethical and regulatory viability of these initiatives. Effective consent management ensures that data used in AI models is transparent, auditable, and aligned with customer expectations, preventing misuse while enabling personalization at scale. By embedding consent into the very fabric of algorithmic decision-making, institutions can balance innovation with responsibility -unlocking the full potential of data monetization while safeguarding customer autonomy and trust.

Transparency and trust

Customers must clearly understand how their data is used. Transparent consent builds confidence and increases opt-in rates (benchmarked at 70 - 80% in BFS when value exchange is clear).

Regulatory compliance

GDPR, CCPA, and emerging data privacy laws mandate explicit consent. Weak consent management exposes institutions to penalties and reputational risk.

Personalization effectiveness

Without consent, personalization initiatives cannot scale. Consent maturity directly impacts the ability to deliver hyper-personalized experiences.

AI governance

In an AI-driven world, consent ensures that personalization algorithms respect boundaries, avoid bias, and align with responsible AI principles.

Effective consent management is not just a compliance requirement - it is a growth and trust lever. In a hyper‑personalized environment, organizations must move beyond static, one‑time opt‑ins to purpose‑led, value‑based consent, where customers clearly understand what they get in return for sharing data. Leading institutions operationalize consent as a core business capability - centrally governed, API‑enabled, and embedded into customer journeys - allowing consent to be activated, adjusted, or withdrawn in real time as use cases evolve. When consent is treated as a monetizable enabler rather than a legal afterthought, it improves opt‑in rates, accelerates personalization adoption, reduces regulatory risk, and builds durable customer trust - making responsible data usage a competitive advantage rather than a constraint.

Example: DBS embedded consent into digital platforms and decisioning.

What DBS did

DBS treats consent as a platform capability, not a channel feature - embedded directly into digibank, open‑banking APIs, and data access layers.

Customer consent for data sharing (e.g., open banking, interbank account data sharing) is managed centrally and exposed via APIs to downstream systems - analytics, personalization engines, and partner integrations.

Customers can view, grant, amend, or revoke consent in real time through the app, and those changes are enforced instantly across systems.

Why it matters from a business lens

Central consent orchestration allows DBS to safely reuse data across new use cases without re‑engineering controls each time.

This has enabled faster rollout of ecosystem partnerships, real‑time offers, and AI‑driven use cases - while maintaining regulatory confidence across markets.

Consent becomes an enabler of speed and scale, not an innovation blocker.

Consent management thus becomes the bridge between innovation and responsibility, ensuring that hyper-personalization drives growth without compromising ethics or compliance.

Select high-impact use cases for BFS

Business area | High-impact use cases | Business outcome/ impact |

Retail banking | Leverage customer transaction data for personalized products and loyalty programs | AI-driven analysis of transaction data increased loan uptake by 15 - 20% |

Lending | Use alternative data (e.g., bill payment history, social signals) for credit scoring and risk | Advanced credit scoring improved SME loan approvals by 25%, reducing default rates by 10 - 12% |

Cards | Monetize spending patterns for targeted offers, dynamic credit limits, and fraud prevention | Personalized card offers boosted customer engagement by 18% and reduced churn by 12% |

Payments | Utilize transaction insights for merchant analytics, real-time fraud detection, and cross-sell | Real-time spend data integration drove 30% higher redemption rates |

Wealth management | Integrate AI and Gen AI for hyper-personalized advisory and cross-sell opportunities | Hyper-personalized robo-advisory services improved portfolio performance by 10 - 12% |

Risk and compliance | Capitalize on claims and behavioral data for predictive risk profiling and monetization | AI-driven fraud detection reduced losses by 30 - 40%, enhancing compliance and trust |

Commercial and investment banking | Use alternative data to enhance credit scoring and unlock underserved segments | Advanced credit scoring models improved SME loan approvals by 25%, expanding market reach |

Open banking /API models | Monetize APIs with real-time data for lending, FX, and payment services | API monetization strategies generated new revenue streams, contributing up to 8% of non-interest income |

Measuring success: “What gets measured gets managed”

Defining KPIs upfront transforms personalization and monetization from conceptual strategies into measurable, scalable, and profitable business practices. Without clear metrics, organizations risk investing in advanced analytics and personalization strategies without understanding their impact on business outcomes.

Industry benchmarks and analyst views

KPI | Industry benchmark (BFS) | Analyst view |

Customer Lifetime Value (CLV) | CLV uplift of 20 - 30% from personalization | McKinsey: Personalization leaders achieve 40% faster revenue growth |

Engagement rate with personalized offers | Personalized campaigns drive 25 - 40% higher engagement | Gartner: Personalization must balance relevance with restraint |

Fraud detection accuracy and false positive reduction | AI reduces fraud losses by 30 - 40% and cuts false positives by 20%+ | Everest: Analytics in fraud monitoring is a trust differentiator |

Incremental revenue from data-driven products | Transaction insights yield 10 - 15% incremental revenue growth | McKinsey: Data-driven product innovation sustains competitive advantage |

Consent opt-in rates and compliance | Transparent value exchange achieves 70 - 80% opt-in rates | Gartner: Consent maturity is key to scaling personalization |

Structured path to value: The CXO playbook

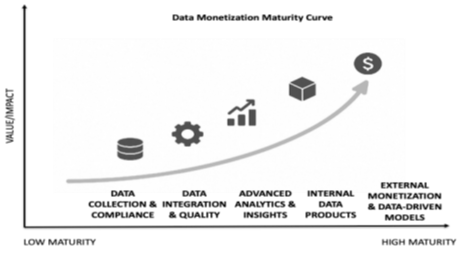

Hyper personalization and data monetization is not a single project but a staged capability build, evolving from compliant data capture to reusable internal data products and, ultimately, external monetization and data-driven business models. Each stage compounds value and risk; advancing prematurely often creates compliance, trust, and scalability issues.

The curve below provides a pragmatic path for organizations to operationalize data as an asset.

Stage | Goal | Typical challenges | What good looks like |

Stage 1: Data collection and compliance | Capture data reliably and meet regulatory obligations. | Siloed operational reporting; ad hoc extracts; fragmented stewardship. | Regulatory readiness: GDPR/CCPA-compliant consent, processing registries, data retention and deletion policies. Foundational governance: Data ownership, lineage, cataloging, classification (PII/PCI), and basic quality checks. |

Stage 2: Data integration and quality | Break silos, enrich context, and ensure high-quality, accessible data. | Centralized lakehouse/warehouse; MDM/Customer 360; role-based access. | Unified entities: Customers, products, merchants, and accounts mastered with survivorship rules. Common reference data: Standardized taxonomies for channels, segments, and risk categories. Reliable pipelines: SLAs for freshness, completeness, and accuracy; automated data quality tests. |

Stage 3: Advanced analytics and insights | Move from descriptive to predictive/prescriptive analytics that change decisions and outcomes. | ML models embedded in processes; experimentation culture; MLOps. | High-impact use cases: Propensity models, risk scoring, fraud detection, next-best-action, price elasticity. Decision integration: Models feed real-time decisioning systems; A/B testing validates uplift. MLOps discipline: Versioning, monitoring (data drift, model performance), and responsible AI governance. |

Stage 4: Internal data products | Create reusable, well-documented data products that internal teams can self-serve. | Curated datasets, metrics-as-code, governed APIs, and domain-aligned data product owners. | Productized data assets: Customer 360 dataset, merchant risk feed, payments performance API. Discoverability and self-service: Cataloged products with clear schemas, sample notebooks, and usage patterns. Operating model: Domain teams own data products; platform team provides tooling (catalog, pipelines, observability). |

Stage 5: External data monetization and data-driven business models | Generate revenue externally and embed data into offerings as a primary value driver. | Data licensing, partner APIs, marketplaces, DaaS/subscription insights, and platform business models. | Monetization models: Tiered licensing, usage-based APIs, premium analytics features, white-label insights. Trust architecture: Anonymization/pseudonymization, differential privacy where appropriate, data usage controls. Ecosystem play: Partnerships with fintechs, merchants, and platforms; co-created products; network effects. |

While successful case studies highlight the transformative potential of data monetization and hyper-personalization, success demands more than isolated pilots.

Building the business case

Financial institutions should approach this initiative with a transformation mindset and build a structured business case that aligns personalization and monetization strategies with measurable outcomes. Without a clear framework, efforts risk fragmentation, failure to scale, and loss of executive sponsorship.

A structured approach ensures that investments in AI, data platforms, and consent management are tied directly to revenue growth, risk mitigation, and customer satisfaction.

Stages | Focus area | Typical owner |

Vision | Objectives aligned with growth, loyalty, and compliance. | Chief Strategy Officer/Head of Transformation |

Platform | Scalable infrastructure, unified customer profiles. | Chief Technology Office/ Head of Data Engineering |

Sources | Integrate first-party, second-party, and third-party data. | Head of Data Management/ Partnerships Lead |

Insights | Advanced analytics and AI for action. | Chief Data Officer/Head of Analytics |

KPIs | Outcomes tied to revenue, risk, and satisfaction. | Chief Marketing Officer/Head of Product/Risk Lead |

Act now

The convergence of market growth, AI-driven personalization, and emerging trends positions BFS firms at the cusp of a transformative era. However, realizing this potential requires more than isolated pilots or proofs-of-concept.

Hyper-personalization and data monetization must be approached as an enterprise-wide transformation program, not a series of disconnected experiments. Why? Because these initiatives touch multiple customer journeys, operational processes, and technology layers across the organization. A cohesive strategy demands cross-functional collaboration, and change management becomes a critical enabler, ensuring cultural alignment and adoption at scale.

Success cannot be measured by vanity metrics, or progress by numbers alone; it must be anchored in well-defined KPIs tied to business outcomes.

When executed holistically, this transformation does more than unlock new revenue streams - it redefines customer relationships, strengthens competitive positioning, and builds a resilient, future-ready enterprise. The question is no longer “Should we?” but “How fast can we move?”